Get The Best Coverage For Less: Cheap General Liability Insurance For Contractors

As a contractor, I know all too well the unpredictable nature of the job. One moment, you're busy at a worksite, focused on the task at hand, and the next, you're faced with an unforeseen accident that results in injury to a client or damage to their property. The financial repercussions of such incidents can be staggering, often reaching tens of thousands of dollars. This is where cheap general liability insurance for contractors becomes not just a necessity, but a lifeline. Many of us, myself included, have underestimated the importance of securing comprehensive coverage, believing that it's out of reach. However, the reality is that with the right approach, you can find the protection your business needs without breaking the bank. In this article, I'll share my personal insights and practical strategies to help you navigate the maze of contractor insurance and secure affordable general liability coverage that fits your budget.

Understanding the Essentials of General Liability Insurance for Contractors

General liability insurance is a crucial safeguard for any contractor, whether you're a solo handyman or the head of a large construction firm. This type of policy covers your business against common risks that can arise on the job site or through your professional services.

Protecting Yourself from the Unexpected

Imagine a scenario where a client trips and falls on your worksite, sustaining a serious injury. Without general liability insurance, you could be left footing the bill for their medical expenses and any legal costs associated with the incident. The average cost of a construction-related lawsuit is around $54,000 - a financial burden that could cripple your business.

General liability insurance can provide coverage for bodily injury, property damage, advertising injuries, and personal injuries that may occur during the course of your work. This means that you don't have to worry about the financial fallout from an unexpected accident or incident.

Meeting Industry Standards

Many clients, especially in the construction industry, won't even consider hiring a contractor who doesn't have general liability coverage. It's a standard requirement for most projects, and not having it can put you at a significant competitive disadvantage.

Furthermore, if you rent a commercial space for your business, your landlord will likely require you to carry general liability insurance as a condition of your lease. It's a safeguard that protects both you and your property owner.

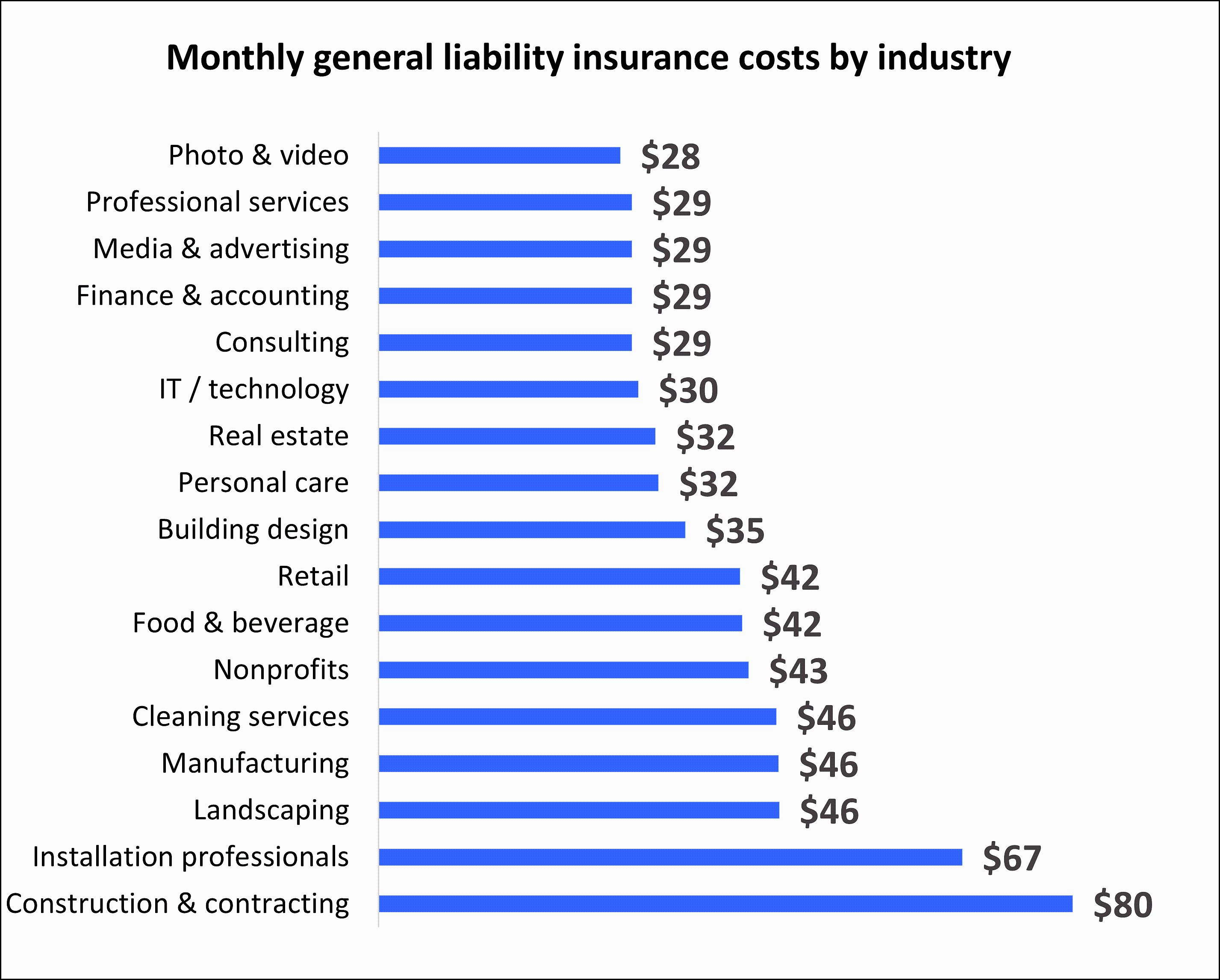

Strategies for Finding Cheap General Liability Insurance for Contractors

While general liability insurance is a must-have for contractors, that doesn't mean you have to overpay for it. By employing a few strategic tactics, you can find coverage that meets your needs without breaking the bank.

Shop Around and Compare Quotes

One of the best ways to save on general liability insurance is to get quotes from multiple providers. Rates can vary significantly between insurers, so it's important to shop around and compare your options.

Online insurance marketplaces like Insureon make it easy to get quotes from top-rated carriers in just a few minutes. Simply fill out a brief application, and you'll receive personalized quotes that you can compare side-by-side.

When evaluating your options, be sure to consider factors like coverage limits, deductibles, and any bundling discounts that may be available.

Negotiate Your Premium

Don't be afraid to negotiate with insurance providers to get the best possible rate. Your experience, safety record, and other risk management practices can all be leveraged to potentially lower your premium.

Start by providing the insurer with detailed information about your construction business, including your years of experience, employee training programs, and any safety certifications you've earned. This demonstrates that you're a responsible, low-risk contractor, which can translate to savings on your policy.

You can also ask about available discounts, such as those for paying your premium annually or bundling your general liability coverage with other policies like workers' compensation or commercial property insurance.

Bundle Your Policies

Speaking of bundling, combining your general liability insurance with other types of coverage can be an effective way to reduce your overall costs. Many insurers offer discounts for contractors who package their policies together.

For example, a business owner's policy (BOP) combines general liability and commercial property insurance into a single, discounted plan. This can be a more affordable solution than purchasing the two coverages separately.

By bundling your policies, you'll not only save money but also enjoy the convenience of having all your business insurance needs managed in one place.

Proactive Risk Management: The Key to Lower Insurance Premiums

In addition to shopping around and negotiating with insurers, taking proactive steps to manage your construction risks can also help you secure lower general liability insurance premiums.

Prioritize Safety on the Job Site

Developing and implementing comprehensive safety protocols is one of the best ways to reduce your risk of accidents and injuries. This includes measures like conducting regular safety inspections, providing personal protective equipment (PPE) to employees, and establishing clear procedures for identifying and addressing hazards.

By demonstrating to your insurance provider that you take safety seriously, you can potentially qualify for discounts on your general liability coverage.

Invest in Employee Training

Proper employee training is another critical component of effective risk management. Ensure that all your workers are well-versed in safety procedures, job-specific skills, and best practices for handling equipment and materials.

Consider partnering with industry organizations or safety training providers to offer comprehensive training programs for your team. Not only will this help protect your employees and clients, but it can also help you negotiate lower insurance rates.

Maintain Meticulous Records

Keeping detailed records of your construction projects, safety inspections, and employee training can also work in your favor when it comes to insurance negotiations. This documentation demonstrates your commitment to risk management and can be used to justify lower premiums.

Invest in construction management software or other record-keeping solutions to streamline this process and ensure that your records are well-organized and easily accessible.

Tailoring Your Coverage to Your Specific Needs

While general liability insurance is a fundamental requirement for most contractors, you may also need to consider specialized coverage options depending on the nature of your work.

Addressing Unique Construction Risks

Depending on the type of construction work you perform, you may need additional policies to fully protect your business. For example, builders risk insurance can provide coverage for materials, equipment, and partially completed structures at your job sites.

Professional liability insurance, also known as errors and omissions (E&O) coverage, can protect you if a client alleges that your work was negligent or failed to meet their expectations. This is especially important for contractors who provide design or consulting services.

Carefully evaluate your specific risks and coverage needs to ensure that your insurance program provides comprehensive protection for your construction business.

FAQ

Q: What is the minimum amount of general liability insurance coverage I need?

The minimum amount of general liability coverage can vary depending on your location and the specific requirements of your industry or clients. However, many experts recommend a minimum of $1 million per occurrence and $2 million in aggregate coverage.

Q: How do I know if I need additional coverage beyond general liability?

Carefully evaluate the unique risks associated with your construction work, such as the use of heavy machinery, the handling of hazardous materials, or the provision of professional services. Speak with an insurance agent to determine if you need specialized coverage like workers' compensation, commercial auto, or professional liability insurance.

Q: What are the common exclusions in general liability insurance policies?

General liability policies typically exclude coverage for employee injuries (which are covered under workers' compensation), damage to your own work or products, and intentional or fraudulent acts. It's important to review the exclusions in your policy to understand what is and isn't covered.

Q: How do I file a claim with my general liability insurance provider?

The process for filing a claim will vary depending on your insurance provider. Typically, you'll need to notify your insurer as soon as possible after an incident occurs, provide any necessary documentation, and cooperate with their investigation. Your insurance agent can guide you through the claims process.

Conclusion

As a contractor, protecting your business from liability risks is essential. By investing in affordable general liability insurance and implementing smart risk management strategies, you can safeguard your company's financial future and focus on growing your construction business.

Take the time to shop around, negotiate with insurers, and tailor your coverage to your specific needs. With the right insurance plan in place, you can have the peace of mind to tackle any job with confidence, knowing that your business is protected.

Remember, the key to finding cheap general liability insurance for contractors lies in a combination of diligent research, effective negotiation, and proactive risk management. By following the strategies outlined in this article, you can navigate the maze of contractor insurance and secure the coverage you need to thrive in the industry.